Introduction: Why Voice AI Compliance Is Non-Negotiable in Financial Services

Financial institutions are deploying voice AI across collections, loan inquiries, account servicing, and customer support at an accelerating pace. According to the 2024 IIF-EY survey of 56 financial institutions, 94% expect third-party AI solution use to increase over the next 12 months. Every one of those voice interactions touches Nonpublic Personal Information (NPI) — and that creates a dual compliance burden most teams underestimate.

Two distinct frameworks govern that burden. GLBA is a federal legal mandate with regulatory enforcement, covering how financial institutions collect, protect, and share NPI. SOC 2 is a voluntary audit standard that has become a de facto enterprise procurement requirement for any vendor that handles customer data.

What follows maps what each framework demands of voice AI deployments, where they overlap, and what technical controls a financial-grade system must have to satisfy both.

TLDR

- GLBA applies to any voice AI system that captures NPI — including call recordings and transcripts containing account or loan data

- FTC Safeguards Rule (2023) mandates encryption, access controls, vendor contracts, and a designated security owner

- SOC 2 Type II validates controls over 6–12 months and is now a standard enterprise vendor requirement

- SOC 2 and GLBA overlap on technical controls but diverge on consumer rights and enforcement

- Self-hosted or private cloud voice AI deployments can eliminate the GLBA vendor oversight obligation entirely

GLBA and Voice AI: What Financial Firms Must Know

The Gramm-Leach-Bliley Act covers banks, credit unions, mortgage lenders, insurance companies, fintech platforms, and lending operations. The obligation is the same across all of them: protect the NPI you collect, maintain, and transmit.

What Counts as NPI in a Voice Call

Under 15 U.S.C. § 6809 and FTC Regulation P (16 CFR Part 313), NPI includes personally identifiable financial information a consumer provides to obtain a financial product or service, or information resulting from that transaction.

In a voice AI context, this captures more than most teams initially assume:

- Spoken account numbers and balances retrieved during a call

- Social Security numbers used for identity verification

- Loan application details, payment history, or overdraft status

- Authentication responses recorded in call audio

- Transcripts that contain any of the above

Call recordings and transcripts are NPI when they contain this type of information — not automatically, but frequently in financial services use cases.

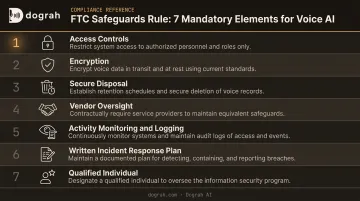

Safeguards Rule (Updated FTC Rule)

The FTC's updated Safeguards Rule (16 CFR Part 314), with amended provisions effective June 2023, requires a written information security program with specific mandatory elements.

The elements that directly intersect with voice AI deployments:

- Access controls limiting who can retrieve call recordings and transcripts

- Encryption of customer information in transit over external networks and at rest

- Secure disposal of NPI no later than two years after last use (unless an exception applies)

- Vendor oversight through written contracts requiring service providers to maintain appropriate safeguards

- Activity monitoring and logging to detect unauthorized access or tampering

- Written incident response plan with documented breach notification procedures

- Qualified individual responsible for overseeing the information security program

The qualified individual requirement has direct implications for voice AI governance: someone in your organization must own the security of voice data, including any third-party system that processes it.

Financial Privacy Rule

Under the Financial Privacy Rule (16 CFR Part 313), financial institutions must provide customers with clear privacy notices describing what NPI is collected and how it is shared — both at the start of a customer relationship and annually.

Voice AI creates two compliance gaps that most legacy privacy notices don't account for:

- New data categories: Call recordings, transcripts, and AI-derived analytics are unlikely to appear in older privacy notices. If your notice doesn't describe how voice data is collected and used, it needs updating.

- Opt-out obligations: Consumers must be able to opt out of NPI sharing with nonaffiliated third parties. A cloud-hosted voice AI vendor that receives, processes, or stores call data can trigger that classification — unless the service-provider exception under 16 CFR § 313.13 applies.

That exception requires an initial privacy notice and a written contract restricting the vendor's use of data to the disclosed purpose.

SOC 2 Type II for Voice AI: The Five Trust Criteria Applied

SOC 2 Type I validates that security controls were properly designed at a single point in time. Type II validates that those controls actually operated effectively over a sustained period — typically 6 to 12 months. For financial services procurement, Type II is the relevant standard. A Type I report confirms a vendor had the right policies on audit day; Type II confirms they maintained them in production.

Security

The Security criterion is the only mandatory Trust Services Criteria in a SOC 2 audit. All other criteria are optional additions based on scope.

For voice AI systems, Security covers:

- Encryption of call recordings and transcripts in transit and at rest

- Multi-factor authentication for platform access

- Penetration testing and intrusion detection controls

- Protection against unauthorized access to voice data and authentication recordings

Availability and Processing Integrity

Availability addresses uptime, failover architecture, and the ability to scale concurrency for high-volume financial call centers. For collections or loan servicing operations running thousands of concurrent calls, this criterion directly governs whether the platform can sustain production load.

Processing Integrity covers transcription accuracy and whether AI decision-making is consistent and free from unauthorized alteration. In regulated call flows — compliance disclosures, authentication, debt validation — transcript accuracy isn't just a quality issue. It's a compliance record.

Confidentiality and Privacy

Confidentiality ensures call recordings, account data accessed by voice agents, and model outputs remain restricted to authorized parties. Privacy requires that data handling aligns with the organization's published privacy notice — including retention schedules and deletion rights.

These two criteria overlap directly with GLBA's Financial Privacy Rule. A SOC 2 audit scoped to include Privacy will examine whether the vendor's data handling is consistent with what consumers were told in their privacy notice — which makes vendor scope selection a meaningful procurement decision, not a formality.

What SOC 2 Auditors Actually Examine for Voice AI

That GLBA overlap is also why auditor scope matters. SOC 2 auditors reviewing a voice AI vendor will look at:

- Data pipeline documentation showing how voice data flows through the system

- Access logs and identity management records

- Incident response documentation and historical response evidence

- Employee security training records

- Sub-processor agreements with downstream vendors

Auditors now routinely ask voice-AI-specific questions: how prompts and conversation history are stored, what controls prevent call data from being used to train third-party LLMs, and what human oversight exists over AI-generated responses. LBMC notes that SOC 2 can address generative AI risks including customer data leakage through training data and model outputs. Auditors provide assurance over the controls surrounding AI — not over AI output itself.

Where GLBA and SOC 2 Overlap — and Where They Don't

| Requirement | GLBA Safeguards Rule | SOC 2 (Security + Confidentiality + Privacy) |

|---|---|---|

| Encrypted storage and transmission | ✅ Required | ✅ Covered |

| Access controls | ✅ Required | ✅ Covered |

| Incident response plan | ✅ Required | ✅ Covered |

| Vendor management via contracts | ✅ Required | ✅ Covered |

| Consumer opt-out mechanism | ✅ Required | ❌ Not addressed |

| Annual privacy notices | ✅ Required | ❌ Not addressed |

| Regulatory examination process | ✅ Subject to | ❌ Not applicable |

| Enforcement | Federal law (FTC, OCC, FDIC) | Voluntary attestation |

A well-scoped SOC 2 Type II audit covering Security, Confidentiality, and Privacy satisfies a significant portion of GLBA's technical control requirements. But the two frameworks diverge on enforcement and consumer rights.

GLBA is federal law enforced by the FTC, OCC, FDIC, and state regulators — non-compliance carries civil penalties and regulatory action, including civil money penalties under 12 U.S.C. § 1818 for banking institutions. SOC 2 non-compliance doesn't trigger fines but will disqualify a vendor from enterprise contracts.

Financial institutions need both — GLBA to operate legally, SOC 2 to clear enterprise vendor due diligence — but the two cannot substitute for each other. A vendor's SOC 2 report leaves three GLBA obligations entirely unaddressed:

- Consumer opt-out mechanisms required under the Privacy Rule

- Annual privacy notices to customers

- Regulatory examination by the FTC, OCC, or FDIC

The financial institution remains directly liable for all three, regardless of what controls its vendors maintain.

Technical Controls Every Financial-Grade Voice AI Must Have

Voice Data Encryption and Segmentation

The FTC Safeguards Rule (16 CFR § 314.4(c)(3)) requires encryption of customer information at rest and in transit over external networks.

NIST SP 800-52 Rev. 2 sets TLS 1.2 as the minimum for data in transit, with TLS 1.3 recommended for new implementations. NIST FIPS 197 approves AES-256 for data at rest.

Platforms like Dograh AI implement TLS 1.3 in transit and AES-256 at rest. In private cloud deployments, this encryption operates entirely within the customer's own infrastructure.

The FFIEC's cloud security guidance also requires logical segmentation in multi-tenant environments — separate privileged credentials per segment, encryption key management, and controls preventing unintentional data interaction across tenants.

Access Controls and Audit Logging

Role-based access control (RBAC) should govern who can retrieve call recordings or transcripts — limiting access to authorized roles only. Dograh AI includes RBAC for transcript and recording access as part of its core platform controls.

The Safeguards Rule (16 CFR § 314.4(c)(8)) requires monitoring and logging of authorized user activity to detect unauthorized access or tampering. The FFIEC Information Security booklet reinforces this with requirements for central logging, timely log transmission, and periodic independent review.

Complete audit logs capture:

- Who accessed or modified data, and under which role

- Timestamps and session context for each access event

- Any configuration changes to retention or redaction settings

Retain logs for a minimum of three years to align with standard FFIEC examination cycles.

PII and NPI Handling in Transcripts

Voice AI generates transcripts that contain raw NPI. Compliant deployments need:

- Real-time PII/NPI redaction from transcripts before storage

- Configurable data retention policies with automated deletion schedules

- Explicit controls preventing voice data from being used to train third-party LLMs

For self-hosted Dograh AI deployments, redaction pipelines can be built into the data flow before storage — giving institutions direct control over what is retained and in what form.

The bring-your-own-keys architecture means user data flows directly to the institution's own chosen providers, not through Dograh's infrastructure as an intermediary.

Incident Response and Breach Notification

16 CFR § 314.4(h) requires a written incident response plan. The FTC's notification amendment — effective May 13, 2024 — requires notice to the FTC no later than 30 days after discovery of a security event involving unauthorized acquisition of unencrypted customer information of 500 or more consumers.

For voice AI specifically, your incident response plan should define what constitutes a breach in this context. Common trigger scenarios include:

- Unauthorized access to call recordings or stored transcripts

- Transcript exfiltration via API or storage layer compromise

- Exposure of authentication recordings containing NPI

Ensure any voice AI vendor has contractually committed to notification timelines that give you enough lead time to meet the 30-day FTC requirement.

Vendor Risk Under GLBA: Why Deployment Architecture Matters

The Service Provider Obligation

16 CFR § 314.4(f) is unambiguous: financial institutions must select and retain service providers capable of maintaining appropriate safeguards, require those safeguards by contract, and periodically assess service providers based on risk.

When a cloud-hosted voice AI vendor receives, maintains, or processes call recordings and transcripts, it fits the service provider pattern under GLBA. That relationship requires:

- A written contract requiring the vendor to implement and maintain safeguards

- Periodic assessments of the vendor's controls

- Ongoing oversight to confirm the vendor's safeguards remain adequate

This is not a one-time check. It's a continuous oversight obligation that extends for the life of the vendor relationship.

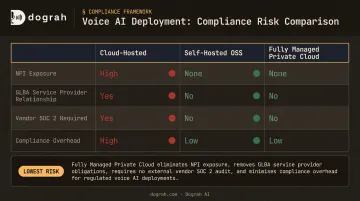

Cloud vs. Private Cloud: The Compliance Calculus

| Deployment Model | NPI Exposure | GLBA Service Provider Relationship | Vendor SOC 2 Required |

|---|---|---|---|

| Cloud-hosted voice AI | NPI transits vendor infrastructure | Yes — contracts and oversight required | Yes |

| Self-hosted OSS | NPI stays in customer infrastructure | No — institution controls its own systems | No |

| Fully managed private cloud | NPI stays in customer's environment | Significantly reduced or eliminated | No |

Cloud-hosted voice AI routes NPI through a third-party vendor's infrastructure. That creates the GLBA service provider relationship, with all the contractual, audit, and ongoing oversight obligations that follow.

A self-hosted or private cloud deployment keeps NPI within the financial institution's own infrastructure. Dograh AI's fully managed private cloud builds and deploys the entire voice agent stack within the customer's own cloud environment, managing orchestration, upgrades, and operational overhead while ensuring data stays on-premise.

With locally hosted STT models (Whisper, Canary) and LLMs (Llama, Mistral) running inside the customer's environment, voice and transcript data never leaves the institution's infrastructure. The compliance outcome:

- No third-party data exposure

- No service provider relationship to manage under § 314.4(f)

- No vendor SOC 2 report to review and maintain in your oversight file

Procurement Efficiency

Vendor SOC 2 reviews are time-consuming. A SOC 2 Type II observation period alone runs 3 to 12 months, with audit and report phases adding additional weeks. For financial institutions looking to go live quickly, the vendor review process is often the longest variable in the timeline.

Self-hosted or private cloud voice AI deployments avoid this process entirely — accelerating go-live without cutting compliance corners.

Frequently Asked Questions

What is a voice AI platform?

A voice AI platform is software infrastructure that enables organizations to build, deploy, and manage AI-powered voice agents for inbound and outbound calling — handling speech recognition, natural language understanding, and response generation at scale. Dograh AI, for instance, is an open-source, self-hostable platform that covers the full voice agent stack without vendor lock-in.

What is an AI SOC platform?

In compliance contexts, "SOC" refers to Service Organization Control — specifically SOC 2, a security and privacy audit framework from AICPA. Voice AI vendors use SOC 2 reports to demonstrate that their data handling controls meet enterprise-grade standards. It is not related to a Security Operations Center (SOC) in the cybersecurity sense.

Will SOC 2 be replaced by AI?

No. AI tools are being used to automate continuous monitoring and evidence collection that supports SOC 2 audits, but the independent third-party audit requirement remains unchanged. Automated compliance tooling accelerates preparation; it does not replace the audit itself.

Does GLBA apply to voice AI systems used by financial institutions?

Yes. GLBA applies to any system — including voice AI — that collects, processes, or stores NPI on behalf of a covered financial institution. Both the Safeguards Rule and the Financial Privacy Rule obligations attach to voice AI deployments that handle financial customer data.

What is the difference between SOC 2 Type I and Type II for voice AI vendors?

SOC 2 Type I validates that controls were properly designed at a point in time; Type II confirms those controls operated effectively over 6 to 12 months. Most financial services procurement teams require Type II, since it confirms a vendor's security posture holds in production rather than just at audit time.

Can a self-hosted voice AI deployment simplify GLBA and SOC 2 compliance?

Yes. Self-hosted or private cloud deployments keep NPI within the institution's own infrastructure, eliminating the GLBA service provider relationship under 16 CFR § 314.4(f) and removing the vendor SOC 2 audit requirement from your procurement checklist. This reduces compliance overhead and shortens go-live timelines by weeks or months.