The gap between customer expectations and contact center reality is widening fast. According to Market Research Future, the voice banking market was valued at $4.18 billion in 2024 and is projected to reach $41.16 billion by 2035 — a 23.11% CAGR. That trajectory reflects both the scale of the problem and the urgency of the solution.

This guide covers what AI voice assistants are in a banking context, the measurable benefits banks are seeing, the most valuable use cases, what security and compliance actually require, and how to implement one practically.

Key Takeaways

- Voice banking is growing from $4.18B to $41.16B by 2035 — a 10× expansion in under a decade

- AI voice assistants replace keypad menus with natural conversation, backed by real-time account data access

- Handles everything from balance inquiries and fraud alerts to loan servicing and outbound collections — without adding headcount

- Self-hosted deployments keep customer data on your own infrastructure, eliminating vendor compliance overhead entirely

- Banks can deploy initial voice AI use cases in days, not months, with the right platform

What Is an AI Voice Assistant for Banking?

A banking AI voice assistant is a system that combines three core technologies to handle customer calls through natural spoken conversation:

- ASR (Automatic Speech Recognition) — converts what the customer says into text the system can process

- NLP (Natural Language Processing) — interprets the customer's intent, not just their words

- TTS (Text-to-Speech) — converts the system's response back into spoken audio in real time

The result is a call experience where a customer says "I need to block my card" and the system understands, verifies identity, and executes — without a single keypad press.

How This Differs From Legacy IVR

Traditional IVR is a decision tree that offers numbered options, waits for a keypress, then branches accordingly. If a customer's need doesn't match the menu, they're stuck. Most eventually mash zero until they reach a human.

When Alior Bank replaced its legacy IVR with a conversational voice bot, the change was architectural, not cosmetic. Customers stopped navigating menus and started having conversations. The system interprets meaning, pulls live account data, and resolves requests in a single interaction.

Modern banking voice AI also supports voice biometrics. HSBC's Voice ID, for example, analyzes more than 100 physical and behavioral vocal traits — including pronunciation, tone, and voice pattern — to verify identity without security questions.

Key Benefits of AI Voice Assistants for Banks

24/7 Availability and First-Call Resolution

Voice AI eliminates after-hours service gaps entirely. A customer calling at 2 AM gets the same quality of service as one calling at 2 PM — no hold music, no callbacks, no next-business-day delays.

Sterling Bancorp's AI assistant Skye handled over 2 million customer requests in its first year, resolving roughly 50% of common contact center inquiries — including balance checks and debit card declines — around the clock without agent involvement.

BAI research reports that AI agent assistants in bank contact centers can improve first-call resolution and average call-time metrics by 15% or better.

Cost Reduction Through Automation

High-volume routine inquiries — balance checks, card activations, payment confirmations — consume a disproportionate share of contact center cost. None of them require a human agent.

Sterling's Skye assistant was reported to be doing work equivalent to 100 full-time employees during its early deployment — freeing existing staff to handle escalations, fraud cases, and relationship-sensitive conversations that actually require human judgment.

Scalability During Peak Demand

Month-end processing, tax season, a fraud event affecting thousands of accounts simultaneously — these peak moments break human call centers. Hiring for peak capacity means overstaffing for 90% of the year.

Voice AI scales on demand. Bank of America's Erica averages more than 58 million interactions per month and has surpassed 3 billion total client interactions — scale no contact center headcount could match economically.

Personalization and Staff Optimization

Because voice AI connects to CRM and core banking data in real time, it can greet customers by name, recall recent transactions, and tailor responses to their specific account context. Bank of America reports that more than 98% of Erica users find the information they need through the assistant.

For human agents, the shift is just as significant. With tier-1 volume absorbed by AI, the work changes character entirely:

- Agents handle escalations, disputes, and relationship conversations — not balance lookups

- Reduced repetitive call load lowers burnout and attrition

- Complex interactions get fuller attention, improving resolution quality

- Freed capacity can be redirected to proactive outreach or financial advisory

Top Use Cases of AI Voice Assistants in Banking

Inbound Account and Transaction Services

This is where voice AI delivers the fastest ROI. The highest-volume inbound banking queries are also the most straightforward to automate:

- Account balance and transaction history

- Fund transfers between accounts

- Bill payment scheduling and confirmation

- Deposit status checks

- Card activation, blocking, and replacement requests

- Credit limit adjustments and travel notifications

Bank of America's Erica is the clearest proof point at scale. Having assisted nearly 50 million users and delivered over 1.7 billion proactive personalized insights, Erica demonstrates what a mature banking voice assistant looks like in production. Clients have spent more than 18.7 million hours conversing with it — and Erica has undergone more than 75,000 updates since its 2018 launch.

Card management is particularly well-suited to voice AI. A customer who's lost their card wants to block it immediately, not navigate three IVR menus to find the right option. Conversational voice commands handle this in seconds.

Fraud Detection and Proactive Alerts

Voice AI's outbound capability is often underestimated. When a suspicious transaction is detected, an AI voice bot can contact the customer immediately: confirming identity, verifying whether the transaction is legitimate, and flagging or freezing the card if needed. No agent required, no queue, no delay.

HSBC's Voice ID system demonstrates what voice biometrics add to this picture. By analyzing more than 100 vocal traits, the system can verify a caller's identity faster than any security question workflow, and can detect whether a voice is live or a playback recording to prevent social engineering attacks.

Finextra reported that, as of 2021, HSBC's Voice ID had prevented £249 million in attempted fraud and cut telephone banking fraud by over 50% — a directional benchmark for what voice biometrics can do to fraud exposure.

Outbound Engagement and Loan Servicing

Fraud prevention is reactive by nature. Outbound voice AI flips that equation, reaching customers proactively before problems escalate.

Payment reminders, EMI alerts, and collections outreach can run across thousands of simultaneous calls — each maintaining compliant, professional conversations while automatically logging every response. For collections specifically, this means:

- Disclosure of reason for call and verification of right-party contact

- Sharing due amounts only after identity confirmation

- Offering payment links, extension options, or agent escalation

- Logging promise-to-pay commitments and scheduling follow-ups within frequency limits

- Sending post-call summaries via SMS or email

For loan and mortgage servicing, voice AI handles eligibility checks, EMI calculations, document requirement guidance, and application status updates — routing complex advisory questions to human specialists only when the conversation requires it.

Security, Compliance, and Data Sovereignty in Voice Banking

Regulatory Compliance for Voice AI

Banking voice AI deployments intersect with multiple regulatory frameworks. Understanding what each requires is essential before selecting a platform:

| Framework | What It Requires for Voice AI |

|---|---|

| GDPR (Europe) | Voice data classified as biometric data under Article 9; requires explicit consent, records of processing (Article 30), and right to erasure (Article 17) |

| GLBA / FTC Safeguards Rule (USA) | Written information security program with administrative, technical, and physical safeguards covering customer voice data |

| FFIEC Authentication Guidance (2021) | Risk-based authentication, layered security for higher-risk access, and documented risk assessments |

| SOC 2 Type II | Third-party control assurance across security, availability, processing integrity, confidentiality, and privacy — required for most vendor procurement |

A frequently overlooked procurement cost: when banks use third-party cloud voice AI platforms, every vendor in the data flow requires its own compliance vetting — SOC 2 audits, GDPR Data Processing Agreements, BAA negotiations for any health-adjacent data. This adds months to procurement timelines.

Data Sovereignty and Private Deployment

Customer voice data, transaction details, and behavioral patterns are among the most sensitive assets a bank holds. Sending them to an external AI vendor's infrastructure creates a data flow that requires extensive ongoing audit.

This is why banks with strict data governance requirements are increasingly opting for self-hosted or private cloud voice AI deployments, where data never leaves the bank's own infrastructure.

Dograh AI is built specifically for this requirement. As an open-source, self-hostable platform (BSD 2-Clause license), it offers fully managed private-cloud deployments where all voice interaction data stays within the bank's own environment — with zero external data transfer.

Because Dograh never sits in the data path, banks skip several procurement bottlenecks entirely:

- No Business Associate Agreement to negotiate with the platform vendor

- No SOC 2 audit cycles to wait on

- No GDPR Data Processing Agreements required for the voice AI layer

The practical result: internal security reviews and direct provider vetting run in parallel rather than waiting on platform vendor compliance documentation. The codebase is fully auditable — no black boxes — which matters directly when an auditor asks who can access a given piece of PII.

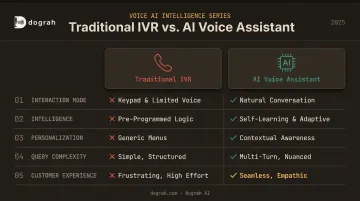

IVR vs. AI Voice Assistant in Banking: Why the Upgrade Matters

| Dimension | Traditional IVR | AI Voice Assistant |

|---|---|---|

| Interaction Mode | Fixed keypad menus | Natural spoken conversation |

| Intelligence | Rule-based, scripted | AI-driven intent recognition |

| Personalization | None | CRM and account data integrated |

| Query Complexity | Simple, pre-defined | Complex, dynamic, contextual |

| Customer Experience | Frustrating, rigid | Conversational, efficient |

Customers who hit dead ends in IVR menus don't wait patiently — they abandon the call, contact a competitor, or file complaints. For banks, this is a direct retention risk. According to The Financial Brand citing Salesforce research, 51% of banking customers cite digital experience as the primary reason for switching providers.

The operational case for upgrading goes beyond customer satisfaction. Traditional IVR systems carry significant maintenance burdens:

- Require manual reprogramming for every policy change

- Can't adapt to new use cases without engineering effort

- Offer no learning capability — performance stays flat over time

AI voice assistants flip this model. They improve with usage, adapt dynamically to new intents, and support a growing range of use cases without complete system overhauls.

Erica has undergone more than 75,000 updates since 2018 — not by rebuilding the system, but by iterating on a learning platform.

How to Implement Voice AI in Your Bank

Implementation Steps

- Define your highest-volume call intents — Start with balance inquiries, card services, and payment questions. These are high-frequency, low-complexity, and deliver measurable ROI quickly.

- Map conversation flows — For each intent, define the full dialogue path: authentication, data retrieval, resolution, escalation.

- Select a platform with secure API integration — Priority criteria: real-time access to core banking and CRM data, compliance-ready deployment options, and documented integration connectors.

- Train and test with real interaction data — Use actual call transcripts to train intent models. AI-to-AI testing frameworks can simulate real-world customer scenarios before go-live.

- Monitor and iterate — Track right-party contact rate, first-call resolution, and escalation rate. These three metrics reveal where the AI is succeeding and where conversation flows need refinement.

The Legacy Integration Challenge

Connecting voice AI to older core banking platforms is the most common implementation obstacle. The solution isn't replacing legacy systems — it's building API bridges that enable real-time data access without requiring full overhauls.

Dograh AI connects to core banking systems, card management platforms, loan management systems, KYC providers, and CRMs like Salesforce and HubSpot through webhooks and tool calls. Banks that already have documented APIs for these systems can move quickly. Those without them should prioritize API layer development as a parallel workstream.

Reducing Time-to-Deploy

Solving the integration layer also unlocks faster go-lives. Modern platforms have significantly compressed implementation timelines. Dograh AI's visual, no-code workflow builder lets teams go from zero to a working voice agent in under two minutes — describing the use case in plain English, which auto-generates the initial workflow. Banking-specific nodes handle compliance requirements directly: disclosure scripts with locked content, consent capture, decision routing, and webhook calls to external banking systems.

The platform supports 70+ languages with mid-call language switching — relevant for banks serving multilingual regional customer bases. Speech-to-Speech orchestration via Gemini Flash Live and OpenAI GPT-Realtime-2 cuts end-to-end latency roughly in half compared to traditional STT → LLM → TTS pipelines, keeping response times tight enough that callers don't notice a delay.

Starting with a focused scope — balance inquiries and card services — allows for fast deployment, measurable early results, and a foundation to expand from.

Frequently Asked Questions

What is the most common AI application in customer service for banks?

AI voice assistants and chatbots are the most common applications — automating inbound calls for balance inquiries, card services, fraud alerts, and loan information. They reduce reliance on human agents for routine interactions while maintaining service quality around the clock.

How does voice AI differ from traditional IVR in banking?

IVR requires customers to navigate fixed keypad menus. AI voice assistants understand natural speech, interpret intent, access real account data, and resolve complex queries conversationally, with no keypad input required.

Is voice AI secure enough for banking applications?

Modern banking voice AI uses voice biometrics, multi-factor authentication, encryption, and fraud detection to protect customer data. Self-hosted deployments add a further layer by keeping all voice interaction data within the bank's own infrastructure and removing external vendors from the data path.

What are the most valuable use cases for AI voice assistants in banking?

The highest-ROI use cases are high-frequency, clear-intent interactions that voice AI handles reliably:

- Account balance and transaction inquiries

- Card management and fraud verification

- Loan servicing and payment reminders

- Biometric authentication

How can banks ensure customer data stays private when using voice AI?

Banks can select self-hosted or private-cloud voice AI platforms where all voice interaction data stays within their own infrastructure. This eliminates third-party data sharing and satisfies GDPR, GLBA, and other regulatory requirements without extensive vendor compliance vetting.

How long does it take to implement a voice AI system for a bank?

Timelines vary by scope and platform. Legacy enterprise deployments can take months. Modern platforms with visual workflow builders and pre-built banking integrations, like Dograh AI, can have initial use cases live in days or weeks. Starting with well-defined intents like balance inquiries or card services accelerates that timeline further.